Monday, March 22nd, 2021 and is filed under Alternative Strategy Mutual Funds

What Happened

On Monday, February 22, 2021, the Infinity Q Diversified Alpha Fund (Fund) and its investment adviser, Infinity Q Capital Management (Infinity Q), sought and obtained an order from the Securities and Exchange Commission (SEC) permitting the Fund to suspend redemptions indefinitely. The Fund is expected to liquidate assets and distribute the proceeds to shareholders with the assistance of a third-party valuation service and the oversight of the SEC’s Division of Investment Management[i]. At this time, there is no estimate of when the liquidation and distribution will be completed. Until then, redemptions of Fund shares will remain suspended[ii].

Why It Happened

The Fund invested according to an alternative investment strategy that primarily used complex derivative instruments to derive intended exposures. According to the Fund’s most recent financial statement, this included correlation swaps, dispersion swaps, and variance swaps, among various other contracts. Adding to the complexity, a significant portion of these assets were categorized as Level 3 for which market prices are not readily available[iii]. For such securities, third-party services are required in estimating the fair value for purposes of calculating the Fund’s net asset value (NAV).

Based on information learned by the SEC and shared with Infinity Q, it was determined the Fund’s portfolio manager had been adjusting certain parameters within the third-party pricing model being used to estimate the fair value of the Fund’s swap contracts[iv]. Upon review, Infinity Q released the Fund’s portfolio manager, who is also the firm’s CIO and Founder, and determined that it was unable to value the current positions nor confirm the historical values of the Fund’s swap contracts. Presumably to avoid a “run on the bank” situation, which can lead to depressed prices and further losses for investors, Infinity Q sought the order from the SEC while it enlists the services of an independent valuation firm to calculate an accurate NAV for the fund.

Key Takeaways for Alternative Mutual Fund Investors

Despite the increased regulatory oversight of the mutual fund structure, relative to private funds and hedge funds, financial professionals and investors must exercise caution when using alternative mutual funds (AMFs). This is due to the increased complexity that may be present within the product structure including short positions, derivatives instruments, illiquid investments, and leverage. The complexity broadens the opportunity set of these funds allowing portfolio managers to pursue non-traditional investment strategies that may provide enhanced portfolio diversification, systematic risk reduction, and alternative sources of return. However, they may also increase risk and reduce transparency for investors, as demonstrated by the recent developments in the Infinity Q Diversified Alpha Fund. As such, consider the following:

- Is the strategy comprehendible? If upon reviewing the fund, you are unclear as to what the fund does and why, exercise extreme caution. An overly complicated strategy that cannot be explained is potentially a red flag. Furthermore, if the fund cannot be understood completely, nor can the inherent risks.

- Does the fund make heavy use of derivatives? This alone is not a red flag. Derivative instruments increase efficiencies in capital markets and provide increased opportunity for return[v]. However, they also increase the potential for investors bearing risk they do not fully understand. As such, if you are unable to determine why a fund is investing in the types of contracts they do, or what exposures they provide, exercise extreme caution.

- Alternatives require increased due diligence. The complexity of an AMF calls for increased due diligence[vi]. If research resources are constrained or limited, consider the use of third-party services for education and research surrounding alternative investments. Services may help drive efficiencies in research, improve understanding, and increase regulatory compliance.

iCapital Network[1]

AI Insight by iCapital Network currently offers an AMF platform designed to provide financial firms and advisors a comprehensive tool for research with a focus on education and application (versus an investment rating). The platform is a web-based, subscription service and consists of two main components specific to AMFs:

- Comprehensive fund-level research reports that focus on a qualitative understanding of team, strategy, and process.

- A training and education platform inclusive of an extensive AMF module and strategy specific modules.

The platform focuses on mutual funds with alternative investment strategies consistent with the hedge fund industry. Funds covered by the platform are portfolio oriented and will typically have a minimum 2-year track record and $200 million in AUM.

The platform currently covers the Fund on a limited basis. As part of our fund-level research, we have a tiered system that includes full and limited reviews. The former includes investment due diligence summarized within the report while the latter aggregates only the available public data. Considering the Fund’s developments, the platform is actively pursuing ways to improve our process including an increase in our screening parameters for limited reviews, enhancing the existing derivative contract reporting, and summarizing Level 3 assets within each report.

For more information on the platform, please contact AI Insight Customer Care at (877) 794-9448 ext. 710 or via email at customercare@aiinsight.com.

Infinity Q Diversified Alpha Fund

The Fund sought to generate positive absolute returns by combining risk management with diversified alpha strategies. Per the latest summary prospectus, the four primary strategies included Volatility, Equity Long Short, Relative Value, and Global Macro. The investable universe included global markets across equities, fixed income, commodities, credit, and foreign exchange.

________________________________

Endnotes

[1] Institutional Capital Network, Inc. and affiliates (herein “iCapital Network”)

[i] Securities and Exchange Commission. https://www.sec.gov/rules/ic/2021/ic-34198.pdf

[ii] Infinity Q Capital Management, LLC. http://www.infinityqfunds.com/

[iii] Financial Accounting Standard 157 (FAS 157). https://www.investopedia.com/terms/f/fasb_157.asp

[iv] Securities and Exchange Commission. https://www.sec.gov/rules/ic/2021/ic-34198.pdf

[v] The Economics of Derivatives. https://www.nber.org/digest/jan05/economics-derivatives

[vi] FINRA Investor Alert. https://www.finra.org/investors/alerts/alternative-funds-are-not-your-typical-mutual-funds

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as legal, tax or investment advice, a recommendation, or as an offer to sell, a solicitation of an offer to purchase or a recommendation of any interest in any fund or security offered by Institutional Capital Network, Inc. or its affiliates (together “iCapital Network”). Past performance is not indicative of future results. Alternative investments are complex, speculative investment vehicles and are not suitable for all investors. An investment in an alternative investment entails a high degree of risk and no assurance can be given that any alternative investment fund’s investment objectives will be achieved or that investors will receive a return of their capital. The information contained herein is subject to change and is also incomplete. This industry information and its importance is an opinion only and should not be relied upon as the only important information available. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed, and iCapital Network assumes no liability for the information provided.

This material is confidential and the property of iCapital Network, and may not be shared with any party other than the intended recipient or his or her professional advisors. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital Network.

Products offered by iCapital Network are typically private placements that are sold only to qualified clients of iCapital Network through transactions that are exempt from registration under the Securities Act of 1933 pursuant to Rule 506(b) of Regulation D promulgated thereunder (“Private Placements”). An investment in any product issued pursuant to a Private Placement, such as the funds described, entails a high degree of risk and no assurance can be given that any alternative investment fund’s investment objectives will be achieved or that investors will receive a return of their capital. Further, such investments are not subject to the same levels of regulatory scrutiny as publicly listed investments, and as a result, investors may have access to significantly less information than they can access with respect to publicly listed investments. Prospective investors should also note that investments in the products described involve long lock-ups and do not provide investors with liquidity.

Securities may be offered through iCapital Securities, LLC, a registered broker dealer, member of FINRA and SIPC and subsidiary of Institutional Capital Network, Inc. (d/b/a iCapital Network). These registrations and memberships in no way imply that the SEC, FINRA or SIPC have endorsed the entities, products or services discussed herein. iCapital and iCapital Network are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2021 Institutional Capital Network, Inc. All Rights Reserved.

Tuesday, December 22nd, 2020 and is filed under AI Insight News

AI Insight CEO Sherri Cooke discusses her key reflections for 2020 including how alternative investments played an important role in portfolios and the impacts of Reg BI. She also shares what’s anticipated in 2021. Read the narrative below or listen to the podcast here.

Sherri formed AI Insight in 2005 with the primary goal of providing the financial planning community with a more efficient and consistent way to access factual information on alternative investment programs – and from that vision the AI Insight database was born.

Q: What are some of the key reflections you have about 2020 and some points of interest for the coming year?

SC: I would say as a ADISA Board member, I was fortunate to be able to spend quite a bit of time this year collaborating with others in the alternative investment industry focusing on some of the things we can do to make the industry better – and to increase the awareness and understanding of these products within a growing audience. I believe we all have to work together to bring this space to a whole new level. Also, as Reg BI requirements continue, we’re looking at ways to partner with compliance and technology workflow companies that are helping to support these needed processes. We’re also looking to connect with other companies – both inside and outside the traditional alternatives space to further increase consistency and transparency in the industry with an ultimate goal of making it easier to conduct alts business.

Q: How do you think alternative investments played an important role in portfolios this past year, especially given the pandemic?

SC: We’re always looking for ways to give more to people – who are of course qualified – access to alternative investments to help them really diversify their portfolio in a meaningful way. Our belief is that a person isn’t fully diversified if all of their underlying investments are either in some way tied to the markets or are invested in a fixed income security – which is effectively still tied to the market.

Despite the pandemic – and in some cases as a result of – there are a lot of really solid opportunities to invest in real assets, interesting investment structures, and institutionally supported opportunities through alternative investments that really provide true diversification.

That said, alternatives can certainly be complex and they need to be factually understood and appropriately sold. This industry really needs to educate financial professionals and investors in so many different ways. One of those has to be around creating realistic expectations about what these investments are intended to bring to a diversified investment portfolio…and what they are not. Stocks lose value all the time and there will be alts that don’t perform. As an industry, we really need to do our very best to ensure that these products are properly sold and positioned within client portfolios. And – as with all investments – we support conducting the best possible research and diligence to allow firms and advisors to select best of class – and help the vested financial firms and producers drive product sponsors toward best of class practices.

Q: We know that compliance is often an issue for advisors in considering alternative investments – and regulatory scrutiny continues to increase. The SEC’s Regulation Best Interest implementation took place on June 30. How does AI Insight help streamline Reg BI requirements?

SC: Compliance is one of the things that motivated me to create AI Insight in the first place. I wanted to build capabilities to facilitate due diligence and proper compliance along with education and documentation of these efforts when selling complex products – those products that the regulators have called out as needing heightened supervision or training.

From an audit perspective, we’ve found in any situation of which we’re aware with our clients, if a firm has stayed up-to-date on the requirements around selling different types of investments – and makes sure everyone involved is aware of their obligations, adheres to the processes, and documents their efforts – then the regulators are generally satisfied. If you fail to make these efforts up front and you’re inconsistent in how you conduct your business from a compliance perspective….you’re just leaving yourself open to trouble.

Reg BI – within the BD community – and I think even though the fiduciary standard has always applied RIA space – we’re going see a whole new layer of extra scrutiny in this regard. The processes that have been central to our platform for years can help support Reg BI requirements and help financial firms and professionals demonstrate the “good faith and reasonable efforts” that Reg BI requires on an ongoing basis. Specifically, we’ve created a comprehensive Reg BI Guide that steps through the Compliance and Care Obligations and correlates the AI Insight support resource to that particular SEC requirement. Again, this is just another way that we help to create efficient and consistent educational and compliance workflows that can help firms at both the product and the firm level.

Q: What is your focus for 2021?

SC: From a business owner’s perspective, ensuring that our team and our product continues to maintain consistent integrity of value and exceptional service; this is the backbone of our business – and making sure that our AI Insight team is challenged and fulfilled in their roles within our company.

From an industry perspective – we believe that there is a tremendous amount of value for advisors to differentiate themselves and bring really great opportunities through the thoughtful and diligent understanding of alternative products. We provide this value by building and bringing together our network of broker-dealers, advisors, RIAs, alternative investment firms and industry partners. Therefore, as in past years, I am always grateful for how far we’ve been able to come and to everyone who has helped us be successful in our efforts to support this industry – and I look forward to working with all of our business partners to explore new possibilities and find what more we can bring to the table for our customers in the new year.

Wednesday, April 29th, 2020 and is filed under Alternative Strategy Mutual Funds

Introduction

As the dust settles from the Corona Market, albeit perhaps temporarily, it is prudent to revisit one’s portfolio and assess the effectiveness of your asset allocation. Diversification is an important component to risk management, and at no time is this better tested than during an equity selloff. Beyond the traditional stock and bond allocation, alternative investments can be an effective way to accomplish this. Broadly speaking, the asset class is designed to provide alternative sources of return to traditional market beta and provide the potential for capital preservation during market drawdowns. As such, it is good to assess the performance of alternatives during these periods to see if the hypothesis holds. Specifically, this piece will focus on alternative mutual fund (AMF) performance through the 1st quarter of 2020. AMFs offer exposure to “hedge fund-like” strategies among other non-traditional approaches within a mutual fund structure. Thus, they can be a liquid and cost-effective means to enhance portfolio diversification.

For the scope of this piece we will define the Corona Market as the equity declines experienced from February 19th through March 23rd. As much uncertainty around the COVID-19 virus and its economic impacts remain, it is important to understand that volatility may persist and that a new low may be established before the drawdown is officially measured. Working with this definition of the Corona Market allows us to make some unique observations about the recent market drawdown.

The Corona Market

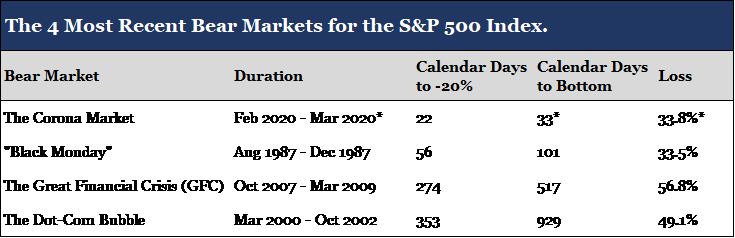

The total loss to the S&P 500 Index, a barometer for US equity markets, amounted to 33.8%. According to data from the CFRA, the average loss experienced during all bear markets dating back to 1929 is 38.2%. Thus, from a historical perspective, the Corona Market was below average in magnitude. However, what made the drawdown so extreme was the speed in which it took place.

*Assumes that the March 23rd index low is the bottom of the Corona Market. Data for the table was sourced from CFRA and S&P Down Jones Indices.

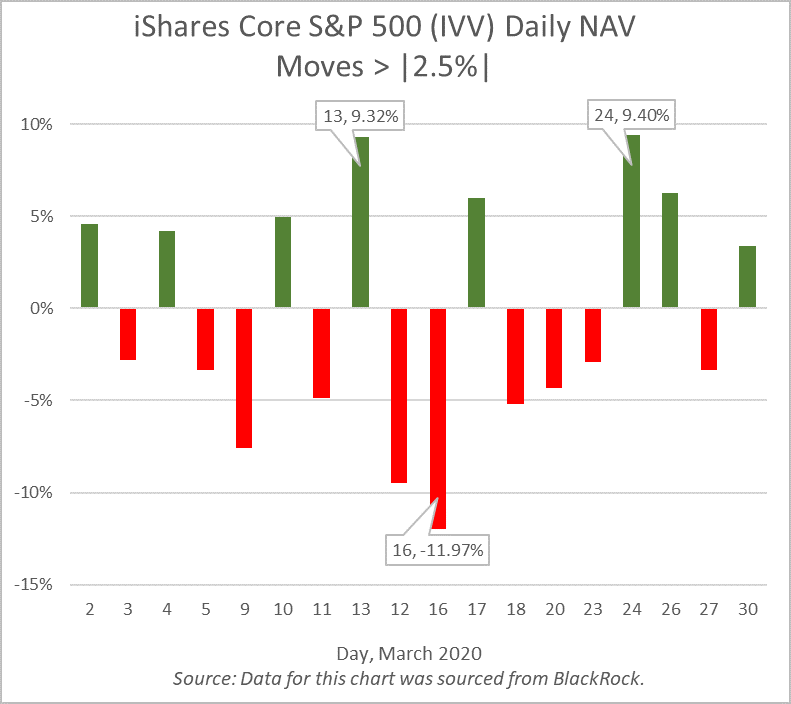

As demonstrated by the table above, the Corona Market decline reached 20% (the definition of a bear market) in 22 calendar days. This is less than half the time it took markets to reach bear territory in 1987 (“Black Monday”) and far below the average of 254 calendar days dating back to 1929. The Corona Market also reached its current low in just 33 days. Such extreme price volatility highlights the uniqueness of a pandemic induced selloff. Taking a closer look, the following chart represents daily NAV changes in excess of +/- 2.5% for the iShares Core S&P 500 ETF (IVV), a passive ETF that tracks the returns of the S&P 500 Index.

The ETF, ticker IVV, had daily NAV moves in excess of +/- 2.5% for 18 out of the 22 trading days in March. This included the March 16th decline of nearly 12%, the S&P’s third largest daily price decline in history (“Black Friday” is the largest daily price decline at -20.5%). As a result, the VIX Index, the market’s forward-looking indicator of volatility, closed at an all-time high of 82.69 the same day.

Alternative Mutual Funds, Passing the Test

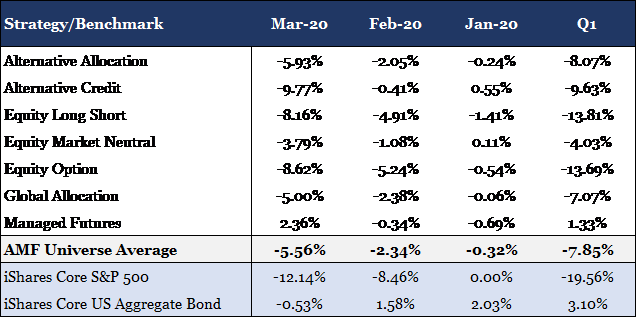

The speed and volatility witnessed during the market drawdown was historic. Working with this understanding of the Corona Market, we can now visit AMF performance for this period within the appropriate lens. The following table represents the performance of the AI Insight universe of AMFs. AI Insight focuses our coverage on funds that execute alternative strategies designed to be held as part (or as all) of an alternative allocation. We also aim to limit our coverage to funds with established track records and sustainable levels of total AUM. The universe is organized into 7 strategy groups, for which the table presents the average performance of each.

The data for the table was sourced from the AI Insight AMF database.

The strongest performer for the period was Managed Futures delivering positive 1.33% through the first quarter. It was the only strategy to remain in the black propelled by a positive 2.36% return during the month of March. Historically, Managed Futures have struggled to capture sharp price reversals as the strategy relies on sustained price trends to build portfolio positions. However, many managers today have increased their weighting toward short term trading strategies and trend signals to better capture downward price swings. This is often referred to as “crisis alpha”, the ability to capture persistent trends that occur across markets during turbulent periods.

Below the AMF universe average for the period were the equity and credit alternative strategies (e.g. Equity Long Short, Equity Option, and Alternative Credit). These funds will typically have higher exposures to risk assets, and as a result, a higher correlation to traditional markets. Furthermore, it is possible the orientation of this market crisis (virus induced shutdown) may have led managers to be more aggressive than they otherwise would have been in a low growth and/or fundamentally weak economy. Prior to the selloff, the financial health of companies and consumers was considerably stronger than what was seen in 2008.

One exception to the equity alternative strategies was Equity Market Neutral. More specifically, the Event Driven sub-strategy of Equity Market Neutral that focuses on mergers and acquisitions among other corporate related events. The sub-strategy was a stronger performer for the period delivering -2.83% performance through the first quarter. These funds are unique in that they invest almost exclusively in equity and equity related securities yet provide a low beta return profile. The -2.83% return equates to a 16.73% outperformance over the iShares Core S&P 500 ETF for the first quarter.

Conclusion

Overall, AMFs delivered strong relative results during the Corona Market with the universe average outperforming the S&P 500 by 11.71% during the first quarter. This included downside protection for both the month of February and March as the average outperformed the equity index by 6.12% and 6.58% respectively. Strategies performed as expected with the more correlated strategies under-performing the average AMF but still out-performing equities, and the less correlated strategies out-performing both the average AMF and the equity markets.

Consistent with these results was the Alternative Allocation strategy which delivered -8.07% for the first quarter as compared to the -7.85% return for the universe. These funds actively invest across multiple alternative strategies and managers within a single fund, providing broad exposure to alternative sources of return. Similarly, the strategy delivered downside protection in both February and March outperforming the equity index by 6.41% and 6.07% respectively.

As demonstrated during the first quarter of 2020, AMFs provide the potential for increased portfolio diversification and downside protection relative to traditional equities. This may serve to reduce portfolio risk during an equity selloff as witnessed during the Corona Market. As mentioned previously, the current low to equity markets occurred on March 23rd. However, there is still much uncertainty that remains around the COVID-19 virus such as potential treatments and vaccines, how best to re-open the economy, and how we will manage the increased debt load that the government and many companies are undertaking to weather the economic shutdown. Despite these uncertainties, equity markets have stabilized since the March 23rd lows appreciating approximately 27% on the backbone of positive hospitalization trends and historic fiscal and monetary policy measures (the S&P 500 is currently down 12.2% through Friday, April 24th). The road may be long, but as mentioned before, diversification is an effective tool in any risk management strategy.

Friday, January 24th, 2020 and is filed under Alternative Strategy Mutual Funds

If your firm approves all fund company mutual funds, additional due diligence may be needed based on continued regulatory guidance on alternative strategy mutual funds.

_________________________________________________________________________________________

Some financial firms have raised questions about the need for conducting additional research on alternative mutual funds given their complex structure compared to traditional mutual funds. Both FINRA and the SEC have published supporting regulatory detail to help differentiate the need for additional due diligence on alternative mutual funds.

How are you demonstrating your understanding of the complexities of alternative strategy mutual funds?

According to PwC’s recent report, Alternative asset management 2020-Fast forward to centre stage, “In the light of the attention from regulators, asset management firms should enter this new line of business well-prepared from a compliance and organisational standpoint. This includes:

- training

- assessing customer suitability

- marketing and education

- building out compliance and surveillance, and

- robust liquidity risk management.”

Take the first step. Let AI Insight help your firm:

1) Identify potential risk exposure

2) Determine due diligence needs

3) Establish policies and procedures around Alternative Strategy Mutual Funds

Contact us for a complimentary Risk Exposure Analysis to see if your firm may need to conduct additional due diligence on alternative strategy mutual funds.

Related Regulatory References

Training Resources

Friday, November 8th, 2019 and is filed under AI Insight News

We recently released our October Private Placement Insights. Highlights from the report include:

- October private placement activity picked up after a slow September, primarily in the 1031 category.

- Our overall private placement coverage is up year-over-year in terms of new fund coverage and aggregate target raise, led primarily by 1031s and Opportunity Zones, while most other categories remain below last year’s levels.

- Our coverage of hedge funds and managed futures has not expanded in 2019. We discussed this in our September Private Placements podcast. We believe the minimal activity in the hedging and futures space can be attributable to a few factors. One is that funds and fund-of-funds used by many retail firms tend to be larger with a perpetual life that have been around for many years and used as needed. Allocations to hedging and futures strategies also tend to be smaller in the retail channel than the institutional side, so fewer options are available and many use liquid alternatives for these allocations, where we have seen a lot of growth and increased coverage in recent years. Additionally, the strong equity market over the last decade has minimized the focus on hedging and futures strategies.

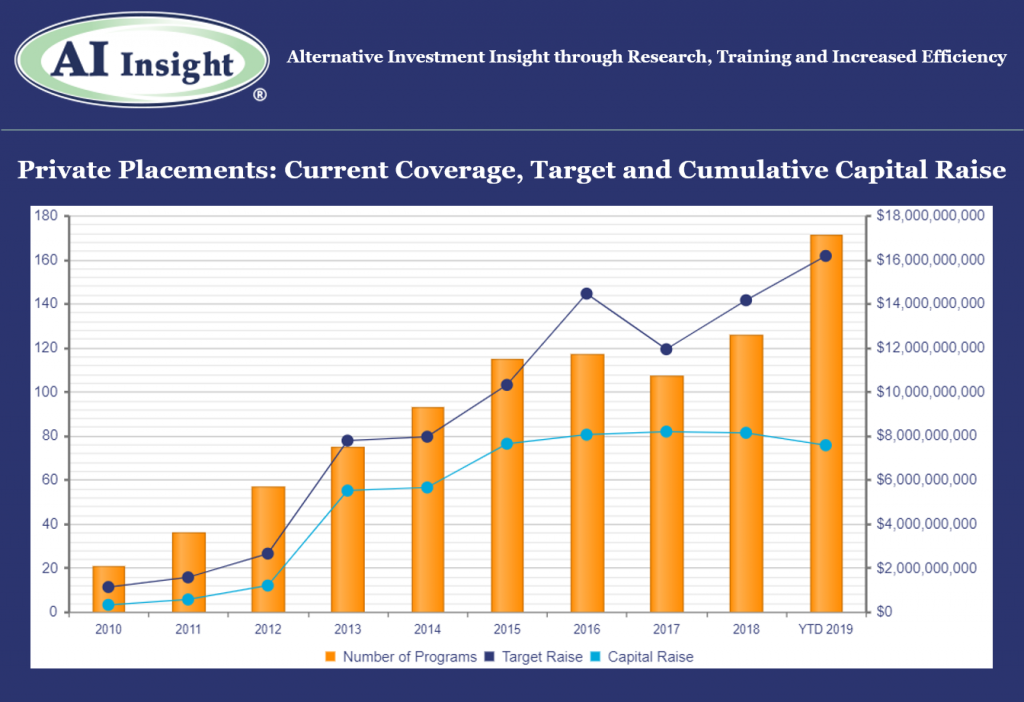

- As of November 1st, AI Insight covers 171 private placements currently raising capital, with an aggregate target raise of $16.2 billion and an aggregate reported raise of $7.6 billion or 46.9% of target. This includes the 147 private placements added to our coverage in 2019.

- As of November 1st, 111 private placements have closed year-to-date which raised approximately 86% of their target raise. While there are still two months remaining, funds this year have come closer to their targets than last year, when the 160 private placements that closed in FY 2018 raised approximately 63% of their target.

Access the full Private Placements report and other hard-to-find alts data

AI Insight’s Industry Reporting capabilities help you review alternative investment trends and historical market data for Private Placements, Non-Traded REITs, BDCs, Closed-End Funds, and Alternative Mutual Funds. Receive up to 24 extensive reports per year to help broaden your alternative investment reviews.

Log in or subscribe to AI Insight to further research, sort, compare, and analyze all of the private and public funds in our coverage universe. See who’s new in the industry and what trends are impacting the alts space.

_________________________________

Chart and data as of Oct. 31, 2019, based on programs activated on the AI Insight platform as of this date.

Activated means the program and education module are live on the AI Insight platform. Subscribers can view and download data for the program and access the respective education module.

On a subscription basis, AI Insight provides informational resources and training to financial professionals regarding alternative investment products and offerings. AI Insight is not affiliated with any issuer of such investments or associated in any manner with any offer or sale of such investments. The information above does not constitute an offer to sell any securities or represent an express or implied opinion on or endorsement of any specific alternative investment opportunity, offering or issuer. This report may not be shared, reproduced, duplicated, copied, sold, traded, resold or exploited for any purpose. Copyright © 2019 AI Insight. All Rights Reserved.

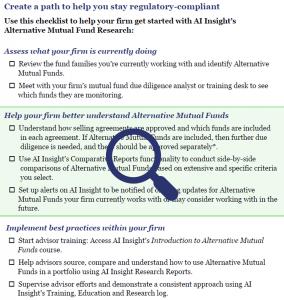

Monday, August 19th, 2019 and is filed under AI Insight News

Have you recently reviewed your policies and procedures around Alternative Mutual Funds? Use the resources below to help your advisors better understand your firm’s best practices. It’s always best to address areas for improvement prior to market corrections, which seem to highlight such deficiencies.

How would you answer the following questions?

- Does your firm approve all fund company mutual funds?

- Is your firm performing the additional due diligence needed based on continued regulatory guidance?

- Does your firm have an efficient solution to establish and enforce best practices?

Related Regulatory References

Watch the video and view this checklist to learn more.

Friday, June 7th, 2019 and is filed under AI Insight News

AI Insight recently added Industry Reporting capabilities to help you review alternative investment trends and historical market data for Private Placements, Non-Traded REITs, BDCs, and Closed-End Funds, and Alternative Mutual Funds. You can receive up to 24 extensive reports per year to help broaden your alternative investment reviews. Read an overview of AI Insight’s expansive coverage as of May 31, 2019:

- AI Insight currently covers 145 private funds that are raising capital, representing just over $5 billion in capital raise/AUM. This includes 20 new funds added to our coverage in May, which was a significant month in terms of new fund formation.

- Five new opportunity zone funds have been added to our coverage YTD, including two in May, for an aggregate target raise of $640.0 million. Target raise ranges from $30 million to $275 million.

- Geographic focus ranges from specifically Maryland to the broader United States. Two funds are blind pool funds focused on hospitality, one is a blind pool fund focused on multifamily, and two are focused on specific mixed-use development projects.

Log in or subscribe to AI Insight to further research, sort, compare, and analyze all of the private and public funds in our coverage universe. Plus, you can view more stats on other private placement categories and access Excel charts of this data.

Watch this tour or request a live demo of AI Insight’s expansive Industry Reports customized to your business needs.

_________________________________

Data as of May 31, 2019, based on programs activated on the AI Insight platform as of this date.

Activated means the program and education module are live on the AI Insight platform. Subscribers can view and download data for the program and access the respective education module.

On a subscription basis, AI Insight provides informational resources and training to financial professionals regarding alternative investment products and offerings. AI Insight is not affiliated with any issuer of such investments or associated in any manner with any offer or sale of such investments. The information above does not constitute an offer to sell any securities or represent an express or implied opinion on or endorsement of any specific alternative investment opportunity, offering or issuer. This report may not be shared, reproduced, duplicated, copied, sold, traded, resold or exploited for any purpose. Copyright © 2019 AI Insight. All Rights Reserved.

Tuesday, May 28th, 2019 and is filed under AI Insight News

Improve your research process using AI Insight’s Alternative Mutual Fund Research capabilities. Our alternatives-centric strategy provides comprehensive information covering investment methods to help you apply liquid alternatives in your practice. Watch a short tour

- Conduct Research: Use reports to research quantitative and qualitative data including fund

company, strategy and investment advisor overviews.

- Understand Fund Strategies: Research strategies including managed futures, long-short, market

neutral and alternative allocation.

- Track Performance: Stay current with performance using portfolio-oriented peer groups and

strategy-based benchmarks for comparison insight.

- Grow Your Business: Use tools to expand your knowledge and track your due diligence efforts

to more confidently identify and apply alternative investment solutions.

Friday, February 1st, 2019 and is filed under AI Insight News

FINRA recently issued its 2019 Risk Monitoring and Examination Priorities Letter along with its 2018 Examinations Finding Report. These reports highlight, among other things, the continued focus on client suitability and overconcentration in non-traded investments, and the need for reasonable due diligence for private placements that is well documented.

Specifically, the 2019 Priorities Letter states,

“As always, suitability will remain one of FINRA’s top priorities. This year, some of the specific areas on which we may focus include: (1) deficient quantitative suitability determinations or related supervisory controls; (2) overconcentration in illiquid securities, such as variable annuities, non-traded alternative investments and securities sold through private placements; and (3) recommendations to purchase share classes that are not in line with the customer’s investment time horizon or hold for a period that is inconsistent with the security’s performance characteristics…”

The 2018 Findings Report stated,

“FINRA has observed instances where some firms that have suitability obligations under FINRA Rule 2111 (Suitability) failed to conduct reasonable diligence on private placements and failed to meet their supervisory requirements under FINRA Rule 3110 (Supervision). FINRA Regulatory Notice 10-22 describes the circumstances under which firms have an obligation to conduct a “reasonable investigation” by evaluating “the issuer and its management; the business prospects of the issuer; the assets held by or to be acquired by the issuer; the claims being made; and the intended use of proceeds of the offering.”

Additionally, in the 2018 Findings Report, FINRA outlines the characteristics of firms that have performed reasonable due diligence, and reminds firms conducting due diligence of their obligation to document both the “process and results” of such reasonable due diligence analysis.

Key Takeaways

- Carefully review and understand the specific suitability requirements for each non-traded or private placement program utilized, and ensure that your firm has a documented process in place to monitor the compliance with suitability requirements.

- Perform a “reasonable investigation” of all complex products, focusing on the specific factors outlined by FINRA in the 2018 Findings Report. For further guidance on what constitutes a “reasonable investigation,” review FINRA Regulatory Notice 10-22.

- Document the due diligence process – remember, if it isn’t documented, it was never done.

- If utilizing third party due diligence vendors, ensure that your firm independently investigates any red flags identified, and document your firm’s investigation and findings.

Let AI Insight help you stay Compliant

- Unbiased education: Access product-specific training on the features, risks and suitability for hundreds of offerings.

- Conduct research: Create efficiencies in your due diligence review process using our robust database to source new products as well as analyze and compare hundreds of alternative investment programs, including non-traded programs, private placements, and alternative mutual funds.

- Compliance documentation: Demonstrate what you’re doing to support your firm’s regulatory requirements in a transparent way. AI Insight captures all of the activity your firm members complete within the platform including training modules, offering document reviews and research conducted.

Resources

Tuesday, June 12th, 2018 and is filed under AI Insight News

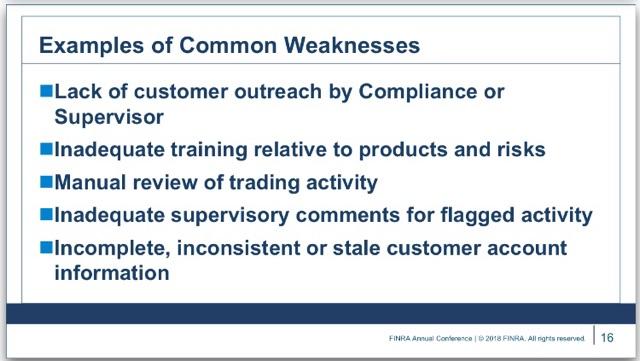

It was great to connect with many of our industry partners at the recent FINRA Annual Conference in Washington, D.C. to discuss regulatory topics relevant to our industry. Here are three key takeaways to consider:

- The industry continues moving forward with a new approach to the standard of care registered representatives must undertake when working with clients. SEC Chairman Clayton was adamant about having industry stakeholders submit comments to help shape the actual outcome of the proposal. He was also quite vocal on the confusion people seem to have around the term “fiduciary” and that he was very much against using it in this proposal. The SEC’s Brett Redfearn provided an overview of Regulation Best Interest and enhancing the standard of conduct for broker-dealers. Read more

- On a suitability panel, “inadequate training relative to products and risks” was noted by FINRA as a common weakness found.

- Heightened diligence and advisor education are needed for the increasingly complex products being offered through traditional ’40 Act structures such as Alternative Mutual Funds and Interval Funds. FINRA mentioned their guidance on complex products as a resource when working with Alternative Mutual Funds, leveraged ETFs, Interval Funds and other alternative investments.