Thursday, April 18th, 2019 and is filed under AI Insight News

It’s important to understand the differences between 1031 Exchanges and the newest alternative investment, Opportunity Zone Funds. While Opportunity Funds and 1031 Exchanges both provide tax deferral mechanisms, there are important differences between the two programs. Read the comparison below, then review the education and training resources available to you.

3 key differences

Tax deferral regulations

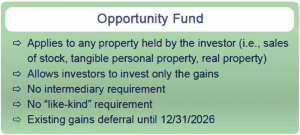

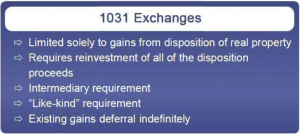

Investors should also keep in mind that gains can be deferred indefinitely through 1031 exchanges. According to proposed regulations, the latest a taxpayer will be able to defer paying taxes on existing capital gains through Opportunity Fund investments is December 31, 2026. Opportunity Funds may provide tax relief for non-qualifying transactions under Section 1031, namely short-term gain property and “blown” I.D. period situations.

Comparison chart

Resources

Content Source: AI Insight CE course, “Introduction to Opportunity Zones”, created in collaboration with Kyla M. Ehrisman, JD, MBA and Alan Lincoln, MBA, CCIM of Mick Law P.C. LLO.